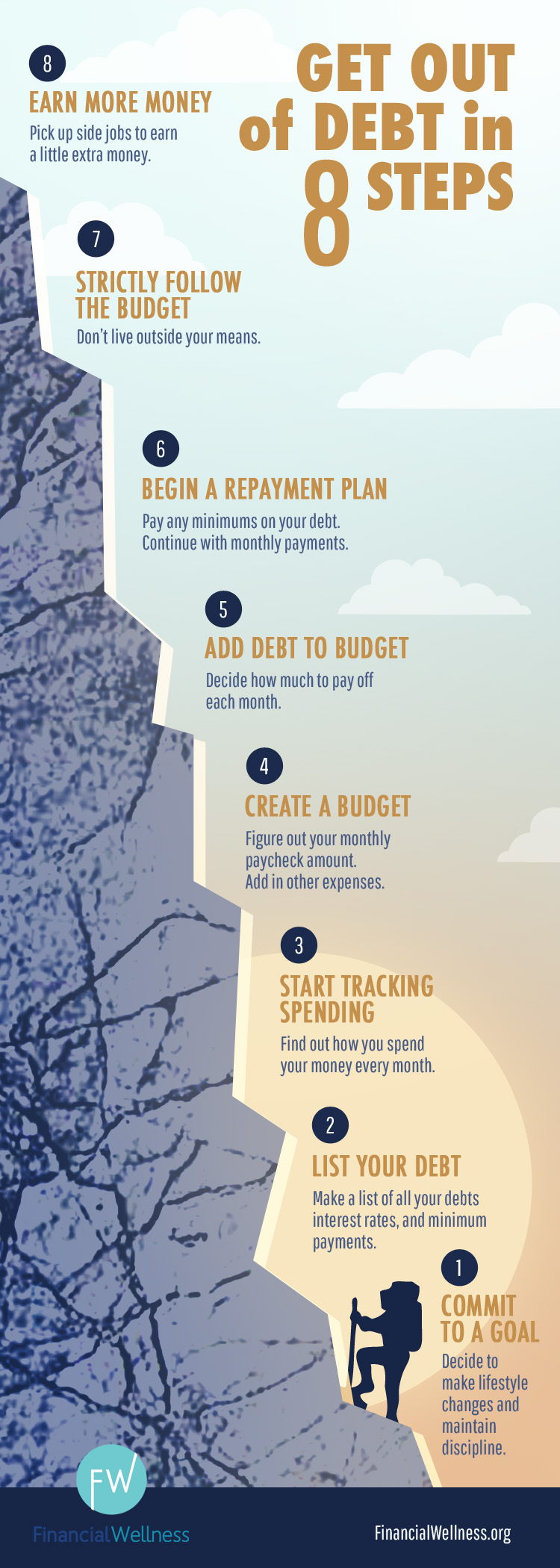

The Main Principles Of Get Out Of Debt

When you miss out on a payment, your loan provider might report it to the credit bureaus-- an error that can remain on your credit reports for 7 years. You might also have to pay late costs, which will not impact your credit report, but can be Click to find out more troublesome nonetheless. Aside from your payment history, the way each type of debt impacts your credit is rather different. Charge card issuers can draw you in with a handle your brand-new charge card account the proper way . The reason revolving debt can be so frustrating is due to the http://www.bbc.co.uk/search?q=debt solutions fact that https://en.wikipedia.org/wiki/?search=debt solutions charge card interest rates are normally really high. So, if you're simply making the minimum payment monthly, it will take you a very long time to pay off your balance-- potentially years.

Let's say you charge $8,000 on a credit card with 17% APR, and then put it in a drawer, never investing another cent. If you make just the minimum payment on that bill each month, it might take you https://www.washingtonpost.com/newssearch/?query=debt solutions nearly 16 years to pay off your debt-- and cost you nearly $7,000 extra in interest (depending upon the regards to your agreement).

If you only have one debt, your method is easy: make the biggest regular monthly debt payment you can handle. Rinse and repeat, up until it's all gone. However if you're like most individuals in debt, you have several accounts to manage. Because circumstance, you need to discover the debt removal technique that works best for you.

We'll explain both of those techniques listed below, along with alternatives like balance transfers, personal loans, and insolvency. We advise using the debt avalanche approach since it's the best method to settle multiple credit cards when you desire to lower the amount of interest you pay. However if that strategy isn't ideal for you, there are a number of others you can consider.

Top Guidelines Of Financial Debt Solutions

Here's how it works: Action 1: Make the minimum payment on all of your accounts. Step 2: Put as much additional money as possible toward the account with the greatest rate of interest. Action 3: Once the debt with the greatest interest is paid off, begin paying as much as you can on the account with the next greatest interest rate.

Whenever you pay off an account, you'll free up more money monthly to put towards the next debt. And given that you're tackling your financial obligations in order of rates of interest, you'll pay less general and get out of debt faster. Like an avalanche, it might take a while prior to you see anything occur.

Let's say you have 4 different debts: Kind of Debt Balance Rates Of Interest (APR) Vehicle Loan $15,000 4.5% Charge card $7,000 22.0% Student Loan $25,000 5.5% Personal Loan $5,000 10.0% To utilize the debt avalanche technique: Always pay the monthly minimum necessary payment for each account. Put any money towards the account with the greatest rate of interest-- in this case, the charge card.

Once the personal loan is paid off, take what you've been paying and add that quantity to your payments for the student loan debt. Once the student loan is paid off, take the cash you've been paying towards other financial obligations and add it to your payments for the auto loan.

The 8-Second Trick For Personal Debt

You'll also have the complete satisfaction of seeing the highest rates of interest vanish. That's why the debt avalanche is our advised approach for settling debt. The downside? It'll typically take longer to see progress than with the debt snowball. So if you're depending on some small wins to get you inspired, the next technique might be a much better fit for you.

Numerous people like this technique because it includes a series of little successes at the beginning-- which will give you more inspiration to pay off the rest of your debt. There's also the possible to improve your credit rating quicker with the debt snowball method, as you lower your credit usage on individual credit cards faster and reduce your number of accounts with impressive balances.

Step 2: Put as much extra money as possible toward the account with the smallest balance. Step 3: Once the smallest debt is settled, take the cash you were putting towards it and funnel it towards your next smallest debt rather. Continue the procedure up until all your debts are paid.

As soon as that's paid off, you concentrate on the account with the next tiniest balance. Think of a snowball rolling along the ground: As it grows, it can get increasingly more snow. Each dominated balance provides you more money to help settle the next another rapidly.

The Facts About Debt Management Revealed

Plus, the debt snowball technique might have a favorable influence on your credit history (specifically if you decide to The original source get rid of charge card debt initially). Better credit can conserve you money in other areas of your life as well. Let's take the same accounts we utilized in the first example. Kind Of Debt Balance Rate Of Interest (APR) Car Loan $15,000 4.5% Credit Card $7,000 22.0% Trainee Loan $25,000 5.5% Personal Loan $5,000 10.0% To use the debt snowball method: Always pay the monthly minimum required payment for each account.

As soon as the personal loan is settled, use the cash you were putting towards it to overcome the next smallest balance-- the charge card debt. As soon as the charge card is settled, take the cash you have actually been paying toward other debts and add it to your payments for the auto loan.

Utilizing the debt snowball approach, you'll end up settling your accounts in this order: Personal Loan ($ 5,000) Credit Card ($ 7,000) Automobile Loan ($ 15,000) Student Loan ($ 25,000) The debt snowball can be an excellent fit if you have numerous little debts to pay off-- or if you require inspiration to settle a great deal of debt.

When you're dealing with a frustrating quantity of debt, this approach lets you see progress as quickly as possible. By getting rid of the tiniest, easiest balance initially, you can get that account out of your mind. Reducing the number of accounts with impressive balances on your credit reports may help your credit rating too.

Some Known Details About Get Out Of Debt

Considering that you don't take rates of interest into account, you could end pay off higher-interest accounts later on. That additional time will cost you more in interest fees. While the debt snowball and avalanche are 2 overarching strategies for how to pay off debt, here are some specific techniques you can use in combination with them.